I have analyzed billions of dollars of legal spend across hundreds of legal departments. Here is what I keep finding, even at the best-resourced ones.

Four to five percent in annual savings. That is it.

Some of these organizations have every imaginable tool. eBilling systems, engagement letters, rate management, outside counsel guidelines, strict adherence to electronic submissions. They have done the work. The savings are still meager.

The basic tactics have become a box-ticking exercise.

So if your CFO has just asked you for a legal spend reduction number, and you are not yet able to give them a defensible answer, this video is for you.

The five dimensions

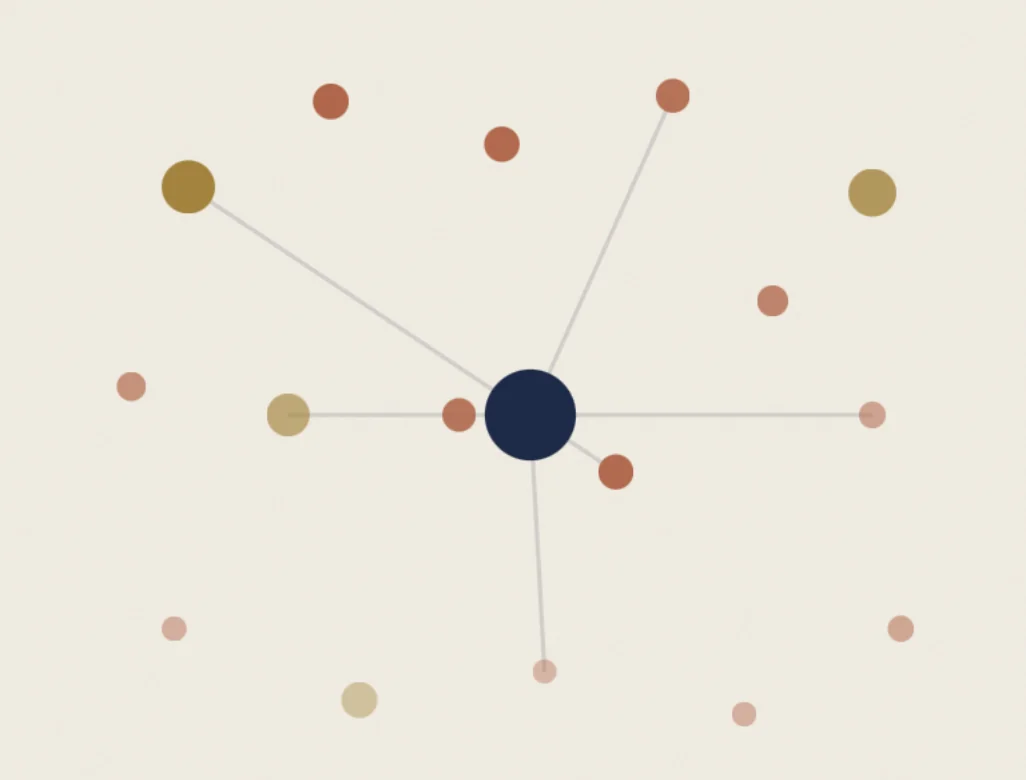

Here is what is actually going on. Outside counsel spend is not a single problem with one cause. It is a five-dimension structural problem. And any reduction effort that addresses fewer than three of those five will leave the spend you could actually recover sitting on the table.

The five dimensions are Panel Architecture, Rate Governance, Invoice Intelligence, Spend Visibility, and Matter Management. Each one is a science in itself.

Fifteen years ago, installing an eBilling system was the trick. You bought it, you turned it on, you were ahead. Today every one of these dimensions is a sports car. Calibrated, fed, tuned, and taken care of every year. Not installed and forgotten.

That is the shift most legal departments have not made. We install the systems, but then we do not have the time to calibrate them properly.

Let me walk you through each dimension. Then I will show you why doing one or two of them in isolation is exactly why your last spend reduction effort underperformed.

Dimension 1: Panel Architecture

Most legal department panels are not built. They grow.

Twenty firms become forty. Predecessor relationships become permanent. A regional preference from 2014 is still costing money in 2026.

The question is not how many firms you use. It is whether your panel reflects deliberate value decisions or accumulated history. When 80 percent of your spend sits with 20 percent of your firms by design, that is healthy. When it is spread across 40 firms with no tier logic, that is panel sprawl, and it is one of the most expensive forms of inertia in any legal department.

Quick test. Count your panel today. How many of those firms were not on it five years ago? If the answer is most of them, your panel grew. It was not built.

Quarterly reports never catch it. Each individual firm relationship looks reasonable in isolation.

Dimension 2: Rate Governance

This is the one most departments think they have under control. Most do not.

The box-ticking version of rate governance is the annual rate increase. The firm sends a letter. You negotiate it down a few points. Then you move on. Box ticked.

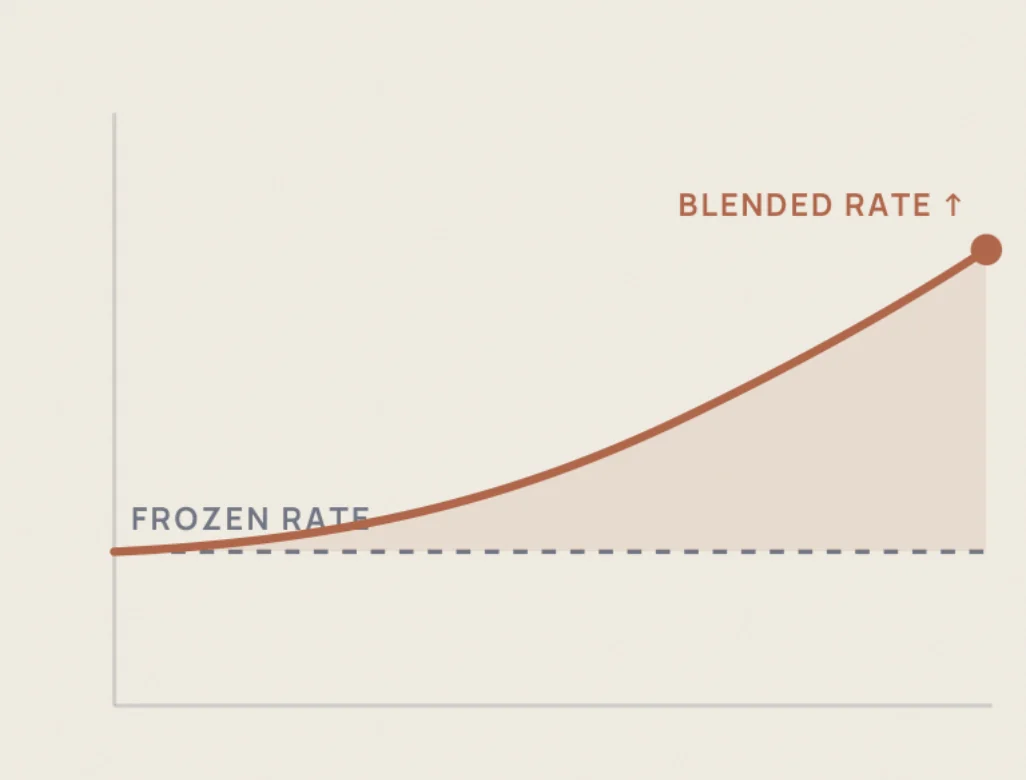

Try this test. Implement a two-year rate freeze with your panel firms. What happens next? Are you then able to confidently say your spend went down?

Did you track the work that shifted to slightly more senior associates whose rates were not frozen? Did you track how many associates were promoted to partner during that time? The frozen rates are technically held, but the blended rate went up anyway.

Here is one I see all the time. A client gets a 10 percent discount on an eleven-hundred-dollar partner rate. Real money on paper. What is not governed so easily is what comes next. Everyone proceeds to use those top-tier firms for all their litigation activity, including the routine commercial litigation that could have gone to a regional firm at 600 dollars an hour. The discount is real. But the structural decision behind it is not governed at all. Saving 10 percent on a rate you should not have been paying in the first place is the real question.

Rate governance is the calibration system around the negotiation.

A quick word

Quick interruption. If, by the time we get to the end of this, you would like me to actually map your specific situation across all five of these dimensions, that is what the CURRENT Assessment is for. Forty-five minutes, on a Zoom call with me directly. No preparation required, no data to pull. Free.

The link is below. Back to it.

Dimension 3: Invoice Intelligence

Quick refresher. Five dimensions: Panel Architecture, Rate Governance, Invoice Intelligence, Spend Visibility, Matter Management. We have covered the first two. This next one, Invoice Intelligence, is where most of the value leakage actually happens. And where AI is being applied to entirely the wrong problem.

There are dozens of structural signals buried inside invoice data, signals that should be feeding decisions in the other four dimensions. Which firms are creeping on rates? Which matter types are running over scope? Which partners are routinely reassigning work to higher-billed associates? Which categories of work are being routed to premium firms when they should not be?

The problem is that bill review is exhausting. You may be reviewing hundreds and thousands of line items per quarter. The job of getting them approved is so consuming that the intelligence inside them never gets extracted.

And the AI tools showing up in this space are mostly not solving the most valuable problem. They are speeding up the approval workflow. They get the invoice approved faster. They do not feed the strategic loop.

The version of this that actually works is invoice analysis that surfaces structural patterns. What your spend is actually telling you about how your panel is performing, where your rate governance is leaking, where your matter management is breaking down. That is invoice intelligence. The current state in most departments is invoice processing.

It is not the firms billing the wrong way. It is the controls around billing not feeding back into anything else.

Dimension 4: Spend Visibility

You cannot manage what you cannot measure. Every GC has heard that. Most departments still struggle with it.

Here is the test. Your CFO drops a question into Slack. “What is our M&A spend this quarter, by firm, against the budgeted number?” How long does it take you to answer with confidence?

If the answer is “I will get back to you in three days,” you are managing reactively from incomplete information. Every reduction target you commit to in that state is a guess dressed up as a number.

If the spend is not consolidated across matter types and business units, if budget-versus-actual is not tracked at the matter level, if the dashboard exists but the data behind it is unreliable, you do not have spend visibility. You have spend reporting. Different thing.

Dimension 5: Matter Management

This is the strategic allocation dimension. It is the hardest to fix because it requires upstream gatekeeping inside the department, and the practice leads do not want a gatekeeper.

The question is whether the right work is going to the right resource at the right cost. Or whether work flows directly from the practice teams to expensive external firms with no triage, no scoping, no internal-versus-external allocation decision.

Run this. The last three matters your team sent out. Who picked the firm? Was there a triage step? Or did the work flow to whoever the practice lead already used?

Most departments have ALSPs, contract lawyers, secondees, and managed-services options on paper. Few have them in the actual decision tree when a new matter walks in the door.

This dimension is the one that quietly defeats most reduction efforts. You can negotiate rates and tighten guidelines all you want. If the wrong work is going to the wrong firm at the wrong cost, you are optimizing the price of a problem you should not be paying for in the first place.

Why most efforts fall short

If you go back and read those five again, the failure mode becomes obvious.

Negotiate rates without addressing Invoice Intelligence, and the savings get absorbed within 18 months by line items nobody is checking. Implement eBilling without updating the outside counsel guidelines, and you get automated payment, not enforced compliance. Rationalize the panel without fixing Matter Management, and work routes to the same premium firms anyway, because the practice teams already know who they want to call. Fix Spend Visibility but never touch Rate Governance, and you get a beautiful dashboard of spend you cannot control.

The CFO-mandated reduction target is not failing because the GC is not trying. It is failing because the standard tools are designed to address one dimension at a time, and the leakage is happening across all five simultaneously.

The answer is not a bigger tool. It is sequence.

Address fewer than three of these dimensions and you are running a procurement exercise. Address all five, in sequence, and you are running an outside counsel optimization program.

A recent engagement

I recently led a Fortune 500 legal department through a rationalization of its outside counsel program, about 600 million dollars in annual spend. Four moves done in sequence: a redesigned panel of firms, fresh rate negotiations, risk-based work routing, and standardized SOPs across the department.

The hardest part was the routing. It meant sitting with each Deputy GC, practice by practice, to define what type of matter actually carried what type of risk, and convincing them what work did not require partner-level attention, what tasks could move to flat-fee, what could go to an ALSP entirely.

That is the operational and structural layer, and this is where you need the expertise to help make the decisions. An ALSP cannot deliver this level of strategic work. The unit they price does not include the senior-level design work.

Across the assessments we have run, 10 to 21 percent recoverable spend is the typical range for departments that have not had a structural review in the last three years.

It is never the amount being spent. It is the absence of the controls that prevents the savings, the right behaviors, the right outcomes. The right controls.

Who this is for

I want to be direct about who this is and is not for.

If you have been through a structural review in the last 18 months and you are confident in all five dimensions, you do not need a CURRENT Assessment.

If you are looking for a vendor to come in and run a procurement exercise on rates, that is not what we do, and there are firms that do it well.

The CURRENT Assessment is for GCs and Legal Ops Directors at 1 billion to 100 billion dollar companies who have run the standard playbooks, are not getting the savings to hold, and want a structural diagnosis before they commit to another initiative.

Sometimes the assessment tells us a Swiftwater engagement is the right next step. Sometimes the honest answer is no, this can be fixed internally, and here is the order to do it. Either way you walk away with a clearer picture than you had.

Close

So those are the five dimensions. Panel Architecture. Rate Governance. Invoice Intelligence. Spend Visibility. Matter Management. Each one a science. None of them, in isolation, will hold the savings your CFO is asking for.

If you want to map your situation across all five, the link is below. Forty-five minutes with me. Free. No data to pull.

If your CFO has asked for a legal spend reduction number and you do not yet have a defensible answer, that is the conversation worth having.